The Laurium Aggressive Long Short hedge fund has substantially outperformed the local market over more than a decade. I chatted to co-portfolio manager Matthew Pouncett about the strategy behind it.

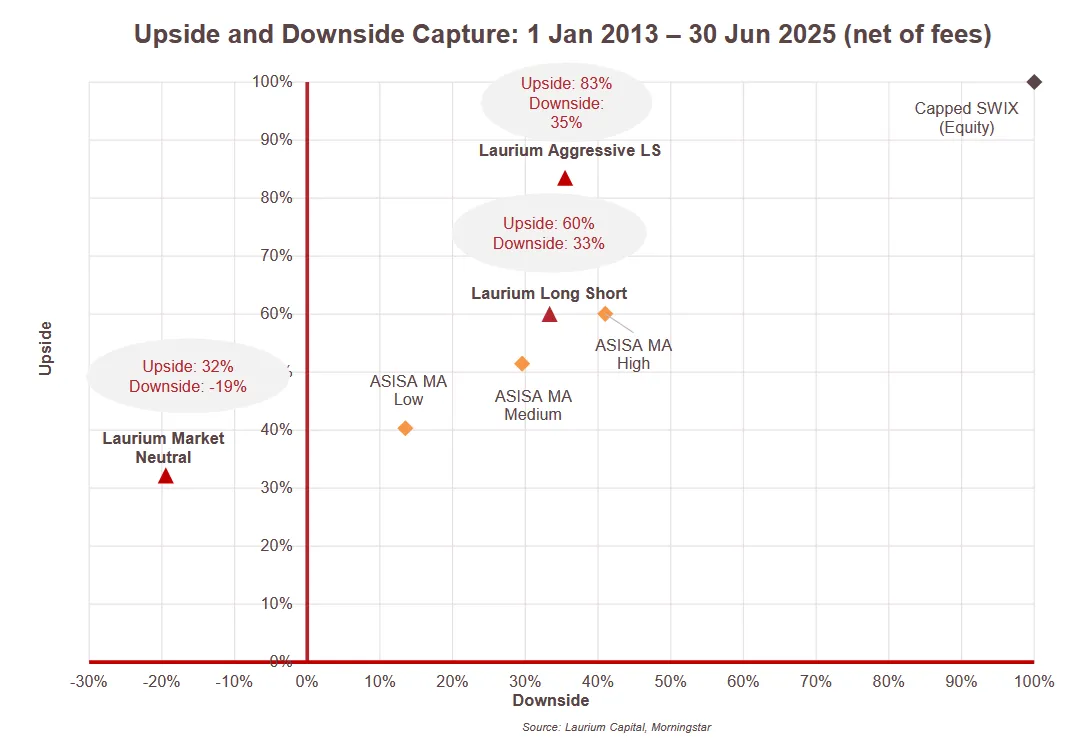

Since its launch just over a decade ago, the Laurium Aggressive Long Short Prescient QI Hedge Fund has delivered a return of 14.8% per year after fees. This is 6.5% per year higher than the ASISA South African equity category average, and 5% per year above the Capped SWIX.

“We think of the Aggressive Long Short hedge fund as an equity replacement,” says co-portfolio manager Matthew Pouncett. “We’ve run the fund with a volatility profile about the same as the market, but with the flexibility of all the hedge fund tools we have at our disposal we’ve been able to enhance the return.”

The strategy, which has been running since January 2013, trades monthly and has a minimum investment amount of R1 million. The Laurium Enhanced Growth Prescient RI Hedge Feeder Fund, which launched in March 2024, follows a similar strategy. It differs in that it offers daily liquidity and may have an allocation to select international equities.

This portfolio feeds into an Irish-domiciled, USD denominated, UCITS fund, launched December 2023. The same fund can therefore be accessed directly by those investors who would like to invest offshore, in USD.

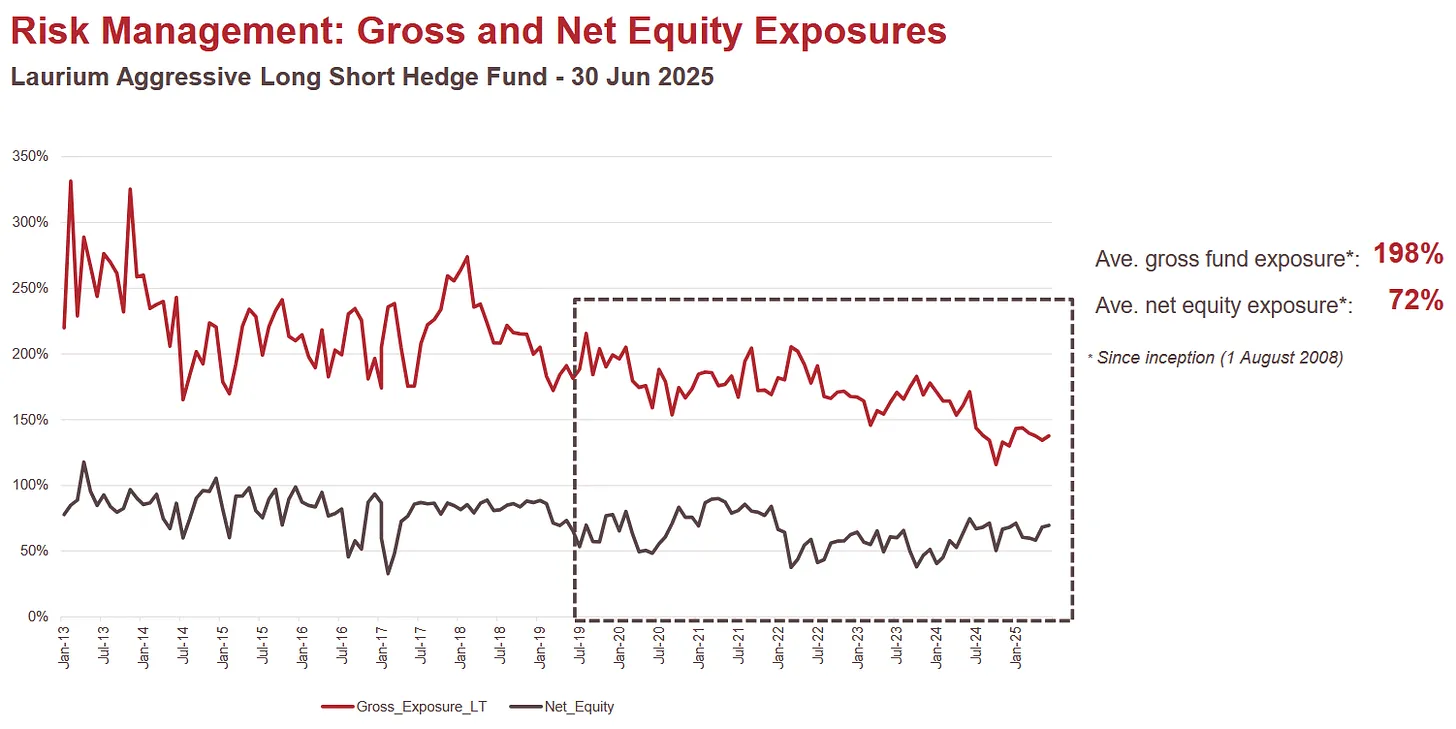

The Aggressive Long Short strategy is run in in conjunction with Laurium Capital’s two other hedge funds – Market Neutral and Long Short – but with higher net and gross exposure limits.

“We run the Long Short hedge fund with a net exposure of around 50%, and there we have a philosophy of wanting to capture two-thirds of the market upside and one-third of the downside upside,” Pouncett says. “In the Aggressive Long Short hedge fund, we are happy to pick up a lot more market beta and will run the net exposure at around 70% or 80% on average.

“Over the life of the fund, we have on average only taken 35% of the downside whilst capturing over 80% of the upside.”

The strategy has an absolute return objective of CPI + 10% over rolling three-year periods. It sits in the Worldwide category, giving it flexibility to invest globally, with offshore exposure averaging around 20%.

“We run the long and short books in conjunction,” Pouncett says. “We want the longs and shorts to be relatively highly correlated.

“If you are running a hedge fund and not considering correlation, you could end up with a book that is, for example, long SA Inc. and short rand hedges, with very large implied currency or sector bets. We always think the short book must be reducing risk – it must not be adding to any factor risk we are running.”

“We are trying to find shares where what the market is pricing in differs from our view.”

The long book is built through Laurium’s bottom-up equity process, focused on finding undervalued earnings and cash generation ability. The short book is put together largely by identifying the inverse.

“We are trying to find shares where what the market is pricing in differs from our view,” Pouncett (pictured below) says. “Sometimes that comes down to aspects of earnings quality like cash conversion, or accounting practices where the market is seeing positive earnings, but we think is overpricing the true cash generation.”

However, he adds that Laurium doesn’t necessarily have to see downside in a share to put on a short.

“A lot of our shorts allow us to upsize a long exposure,” he explains. “For example, we might think a specific insurer is particularly undervalued and at the same time think a sector peer is broadly fair value.

“If we’re happy to run net long exposure to the insurance sector of 5%, we can go 10% long our preferred stock and 5% short the sector peer to get there. That allows us to take more advantage of opportunities on the long side.”

The fund also has a good track record of taking advantage of special situations such as unbundlings, delistings or restructurings.

“We are also never fully invested.”

“The beauty of being able to short is that you can go long and short different components to capture the narrowing of a discount in an unbundling, for example. We are also never fully invested, so have a cash pile to take advantage of things like book builds,” Pouncett says.

“For example, when Ibex sold its Pepkor stake last month, we were effectively short going into the placement, covered that in the placement, and then could go long once the overhang had been removed. We could do that with cash we had available without having to sell anything else.”

On the offshore side, the fund predominantly takes only long positions.

“We look for the portfolio effect of being able to tap into different sectors and thematics that aren’t in existence in South Africa,” he says. “We want to diversify away from sectors we are typically going to be in on the JSE. We are unlikely to buy a UK bank, for example, because banks are a large part of our portfolio locally.

“We rather want to tap into themes like technology or emerging consumer stories that are uncorrelated with our home market.”

“We don’t hold fixed income as a structural position, but we do take opportunities where we think we can get equity-like returns.”

The strategy also has the ability to take advantage of opportunities in other asset classes such as bonds or preference shares.

“We don’t hold fixed income as a structural position, but we do take opportunities where we think we can get equity-like returns,” Pouncett says. “For example, in May 2023 we look a very large position in 10-year South African sovereigns when yields were sitting above 11%.

“Given the coupon and what we believed we could make on falling yields, we thought they could deliver mid-to-high teen returns. We sold out of that position in Q2 this year having gotten that return.”

Article from Running Yield