The best part of being young is that you have your whole life ahead of you. You have time on your side to make mistakes, grow through your experiences and make choices that send you down different paths. As life goes on, however, you realise that time is the one thing you cannot buy (biohacking aside) and the one commodity you cannot get back. Being time rich and money poor may be better than being money rich and time poor, but as always, it depends. One certainty is that the later one starts planning and saving the more likely you are to be both time and money poor.

How often do we hear about wealthy people having to work late into what should be their retirement, either due to a lack of financial discipline, a lavish lifestyle that has got away from them over time or a build-up in debt. A wise bit of advice that is usually handed out to clients is to pay down your debt as soon as possible. A bit of debt is not always a bad thing, depending on where interest rates are and the terms of the debt. This liability does however need to be balanced off by assets, preferably in the form of an investment that can outperform the cost of the debt over time.

Parents typically do their best to provide a sound foundation for their children to have the best chance of success in life. They also tend to pass on their values, their experiences and the practices with which they were raised in their lifetimes. This is usually a positive tailwind to children. Unfortunately, for many parents, the availability and knowledge of investing in their youth was limited. They either did not start young, or at all and have missed the joys of compound interest which has the power to generate real wealth and to strip years off one’s retirement age.

The barriers to entry for a young person to invest have been lowered significantly. It is very simple to open a youth bank account nowadays. It is also easy to open up an investment account at the likes of EasyEquities for your children. Within these platforms, the minimums are insignificant and even the smallest contributions (pocket money) can be invested each month. These can be made into tax free savings investments (TFSA) which will serve the astute savers very well down the line when they get to withdraw 100% of the value of their investment from their account with zero tax obligations.

Parents may donate up to a R100k a year (per parent) to their children without tax implications. This more than covers the R36k limit per person that one can contribute to their TFSA per annum. The TFSA investment option has been available in South Africa since March 2015 (11 years). Over this period a parent could have added R375k to each of their children’s TFSA account. That’s a healthy investment contribution so far, especially if the child is now only 11 years old!

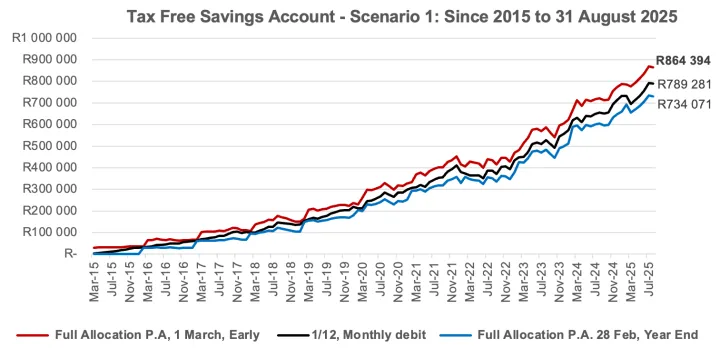

If you had have invested the full yearly allocation into an MSCI AC World Index tracker (ZAR) over the period, you would have grown the R375k over the past 11 years. How you timed your investment also makes a significant difference to the outcome. In the three scenarios’ below, you can see the difference time in the markets has made between adding on 1 March (beginning of the year), monthly (1/12th each month debit order) or last minute.com on 28 February. The early bird option would have made you R130k more to date (R864k).

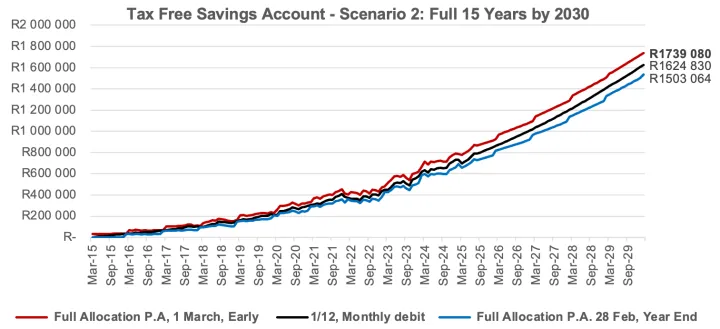

Let us assume the government keeps the R36k annual contribution limit in place and the R500k lifetime limit per person. The parent adds R36k for the next 4 years on 1 March each year and their child reaches his R500k limit at age 15 year. If we assume that the MSCI AC World Equity market delivers the 100yr historical average of 7% real return per annum; CPI is held at around 4% and the Rand depreciates by 3% per annum against the US Dollar (4%+7%+3%=14%) going forward, they will have the value in the chart below by 2030:

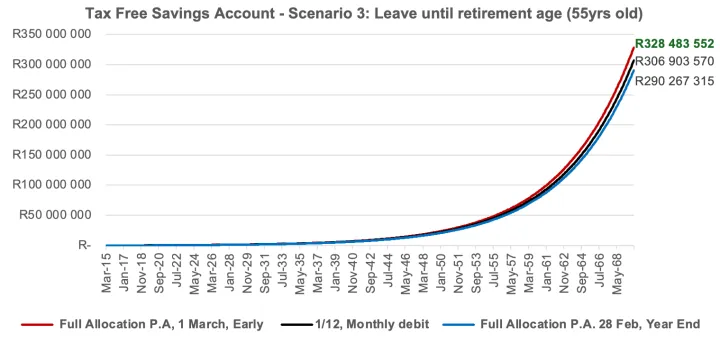

Now let’s pretend the children are not aware of the investment and the parents prefer to leave it as a safety net for their future. This is where the power of compounding really kicks into gear! Without touching it, assuming it grows at the same rate as the last 4 years (14%) into the future, the results are staggering:

In March 2070, in nominal terms, they could have as much as R328mil in their tax free savings account. In today’s terms, the real value (assume 4% inflation) that the 55-year old is now sitting with is R87mil, all of which he/she can withdraw tax free from their investments! And all of this from R500k invested diligently by their parents over 15 years from when they were born. Thanks Mom and Dad!

At Laurium, we believe in ‘Investing for your future!’. Wouldn’t it be great if parents and their children alike, all started investing for their future today. Laurium has recently made the Laurium Global Active Equity Prescient Feeder Fund available via EasyEquities for investment, including the TFSA option! To learn more about Laurium Capital, please contact us today to start your journey.

Article from Daily Maverick